ADHD and Money Problems: The Hidden Connection

Why ADHD and money problems go together, the patterns most people recognise, and a practical starting point that isn't "just make a budget."

If you have ADHD and money problems, you're not alone. And it's not because you're irresponsible. The connection between ADHD and financial struggles is well-documented, rooted in how the brain works, and far more common than most people realise.

Why ADHD and money problems go together

ADHD is fundamentally an executive function condition. Russell Barkley's research identifies executive function as the brain's management system: planning, prioritising, organising, and following through on intentions.

Money management requires almost every executive function skill that ADHD affects:

Working memory makes it hard to hold financial information in mind while making decisions. You forget about a subscription, lose track of your balance, or don't connect today's spending with next week's bills.

Time perception affects how future consequences feel. Thomas Brown's work on time blindness explains why a credit card bill due in three weeks feels abstract, while the thing you want feels urgent now.

Impulse control determines the pause between wanting and doing. When that gap is shorter, impulse spending increases.

Task initiation affects your ability to start boring or overwhelming tasks. Bills sit unopened, budgets never get made, financial admin gets pushed to "later" indefinitely.

This isn't a character flaw. It's a predictable outcome of how ADHD brains process information, time, and reward.

The patterns most people with ADHD recognise

A June 2022 Monzo and YouGov survey found that UK adults with ADHD are significantly more likely to experience financial difficulties:

- 31% are in debt, compared to 11% of neurotypical adults

- 3x more likely to miss payments on bills and credit

- 50% struggle to budget, compared to 15% of neurotypical adults

These statistics reflect patterns that many people with ADHD recognise:

Feast or famine cycles. Spending freely when money comes in, then scrambling when it runs out. The inability to mentally connect current spending with future needs.

Bill avoidance. Knowing a bill exists but being unable to open the envelope or log into the account. The task feels overwhelming, so it gets deferred until it becomes urgent (or goes to collections).

Credit score damage. Not from inability to pay, but from forgetting to pay. Late fees and missed payments that happen not from lack of money but lack of systems.

Debt accumulation. Often from small things compounding: late fees, interest on forgotten balances, overdraft charges. The ADHD tax adds up quietly.

The emotional weight

Money problems carry shame. Financial shame is isolating. It's not something most people talk about openly, which makes it feel like a personal failing rather than a common ADHD experience.

The shame creates a cycle. Feeling bad about money leads to avoiding looking at money, which leads to worse outcomes, which leads to more shame. Breaking this cycle requires separating your financial situation from your self-worth.

ADHD money problems also affect relationships. Partners may interpret missed bills or impulsive purchases as carelessness or lack of caring. Explaining that it's neurological, not intentional, can be difficult when the outcome looks the same.

Recognising the emotional weight is important because it affects what strategies will actually work. Approaches that add guilt or require willpower tend to fail. Approaches that reduce shame and work with ADHD neurology have a better chance.

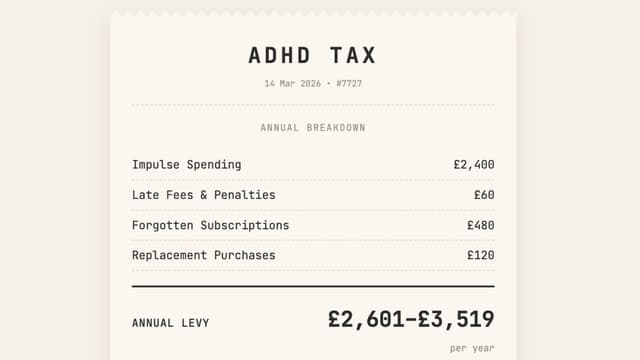

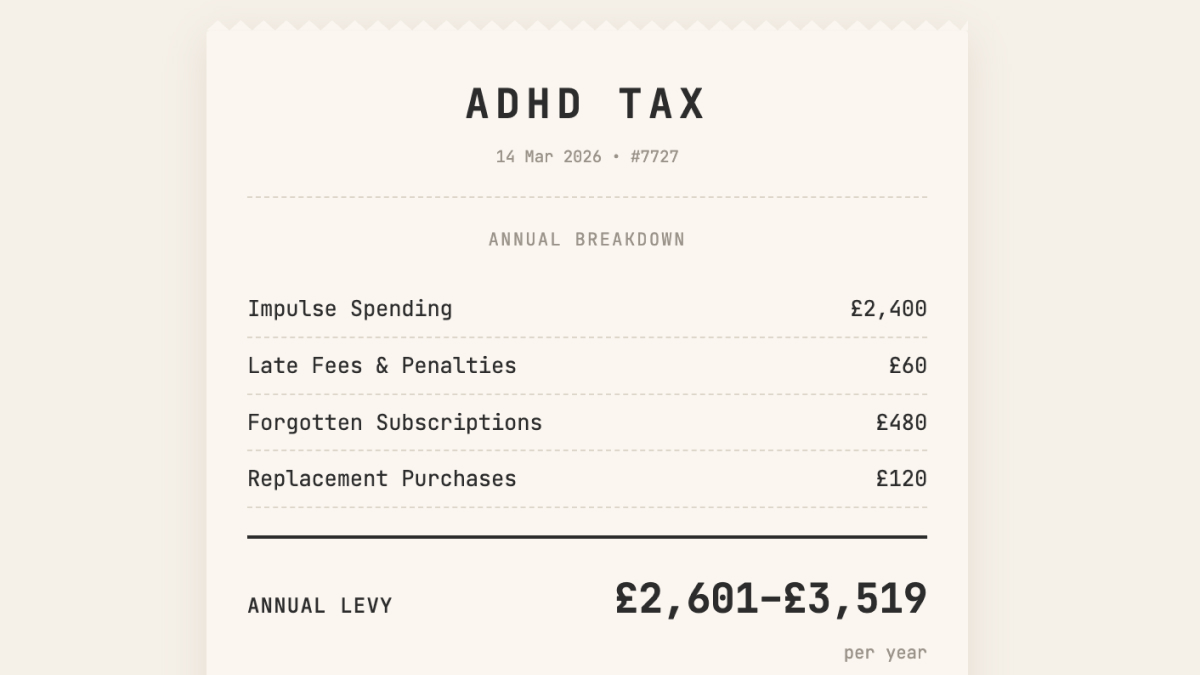

Try the ADHD Tax Calculator

Make the invisible visible. See what ADHD is actually costing you.

Start this toolA starting point that isn't "make a budget"

Generic budgeting advice often fails for ADHD brains. Tracking every expense requires sustained attention. Sticking to categories requires impulse control. Planning for future expenses requires accurate time perception. These are exactly the areas ADHD affects.

A more effective starting point: visibility before restriction.

Before trying to change your spending, simply see it. The ADHD Tax Calculator can help you estimate what ADHD is costing you annually across categories. This isn't about creating guilt. It's about seeing clearly so you can make informed choices.

Once you see the pattern, you can triage. Maybe impulse spending is your biggest cost. Maybe it's late fees. Maybe it's forgotten subscriptions. Each has different solutions. Knowing which one to focus on matters more than trying to fix everything at once.

Start with one category. Pick the one that's costing you most and where change feels achievable. Small wins build momentum. Trying to overhaul your entire financial life at once is a recipe for overwhelm and abandonment.

When to get help

Not all financial help is created equal. Generic financial advisors may give advice that works for neurotypical brains but fails for ADHD.

ADHD coaching focuses on executive function strategies: systems, accountability, working with your brain. A coach who understands ADHD can help you build sustainable financial habits without the shame-based approaches that backfire.

Financial therapy addresses the emotional relationship with money: shame, avoidance, anxiety. If your money problems are tangled up with strong emotions (and they usually are), this can be valuable.

Generic financial advice (budgeting apps, financial planners) can work, but only if adapted for ADHD. Ask whether they have experience with neurodivergent clients. Be wary of approaches that rely heavily on willpower, tracking, or "just being more disciplined."

Whatever help you seek, it needs to account for how ADHD actually works. Strategies designed for neurotypical brains often make things worse, adding guilt without adding capability.

Tools mentioned in this article

Common questions

ADHD affects executive function, the brain systems that handle planning, prioritising, and following through. Intelligence doesn't protect against this.

Yes. Research shows people with ADHD are 3x more likely to miss payments and significantly more likely to carry debt than neurotypical adults.

Generic budgeting advice often fails for ADHD brains. You need strategies designed for how your brain actually works, starting with visibility, not restriction.

Sources & references

- Monzo/YouGov (2022). The Extra Costs of Living with ADHD. Published 27 June 2022.

- Barkley, R. A. (2012). Executive Functions: What They Are, How They Work, and Why They Evolved. Guilford Press.

- Brown, T. E. (2013). A New Understanding of ADHD in Children and Adults: Executive Function Impairments. Routledge.